Advanced Sensor Technologies, AI-Integrated Monitoring, and Remote Patient Care Drive the Next Wave of Growth in Orthopedic Implants

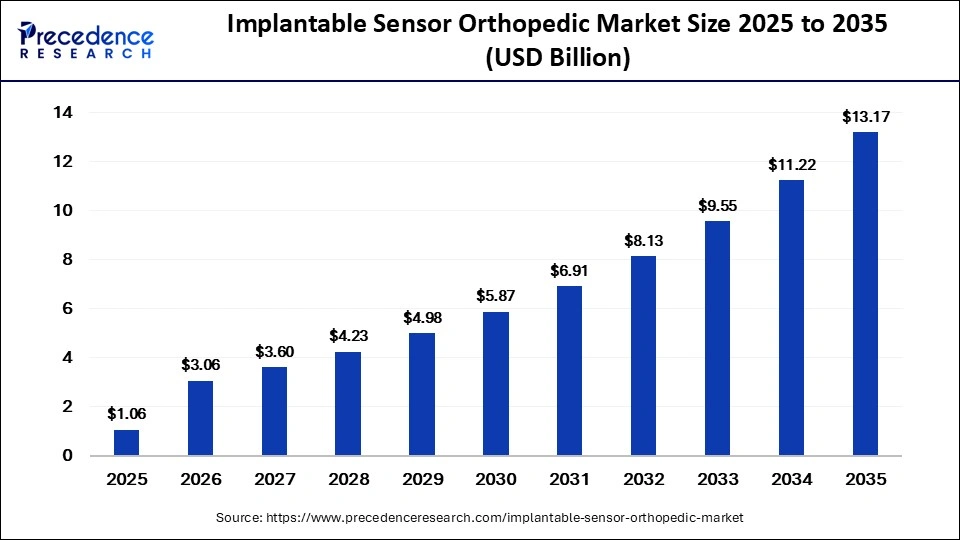

The global implantable sensor orthopedic market is witnessing a significant transformation as healthcare providers increasingly adopt intelligent implant technologies to improve patient outcomes, reduce revision surgeries, and enable continuous monitoring after orthopedic procedures. The market size was valued at USD 1.06 billion in 2025 and is projected to surge from USD 3.06 billion in 2026 to approximately USD 13.17 billion by 2035, expanding at a robust CAGR of 17.04% during the forecast period.

The rapid rise in musculoskeletal disorders, growing incidence of accidents and sports injuries, increasing demand for personalized healthcare, and continuous innovations in implantable sensors are accelerating market expansion globally. Smart orthopedic implants equipped with embedded sensors, wireless communication systems, and AI-driven analytics are revolutionizing how surgeons monitor implant performance and patient recovery.

Implantable Sensor Orthopedic Market Key Points

- The implantable sensor orthopedic market was valued at USD 1.06 billion in 2025 and is forecast to reach USD 13.17 billion by 2035.

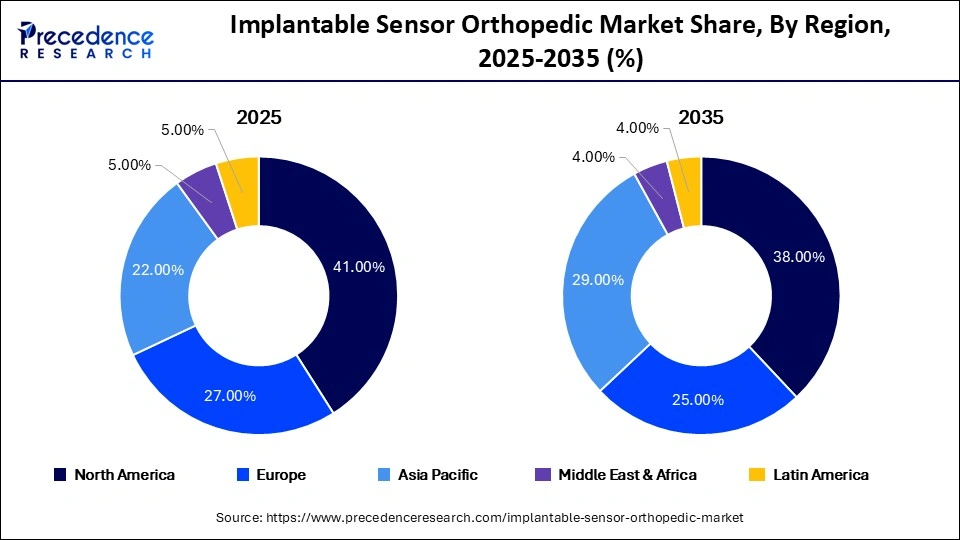

- North America emerged as the leading regional market, accounting for 41% of global revenue in 2025 due to advanced healthcare infrastructure and early adoption of smart implants.

- Asia-Pacific is expected to witness the fastest growth, expanding at a CAGR of 21.2% through 2035.

- Smart knee implants dominated product demand and represented 45% of the market in 2025.

- Pressure sensors generated the highest revenue among sensor categories with a market share of 34%.

- Wireless sensor-enabled implants held the largest technology share of 42% in 2025.

- Joint replacement monitoring remained the leading application segment, accounting for 38% of global revenue.

- Hospitals represented the largest end-user category with a 64% market share.

- AI-integrated monitoring implants are projected to be the fastest-growing technology segment, recording a CAGR of 22.5%.

Implantable Sensor Orthopedic Market Snapshot

| Metric | Value |

|---|---|

| Market Size 2025 | USD 1.06 Billion |

| Market Size 2026 | USD 3.06 Billion |

| Market Size 2035 | USD 13.17 Billion |

| CAGR (2026-2035) | 17.04% |

| Leading Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Leading Product Type | Smart Knee Implants |

| Leading Technology | Wireless Sensor-Enabled Implants |

What Makes Implantable Sensor Orthopedic Devices a Game-Changer in Modern Healthcare?

Implantable sensor orthopedic devices represent a new generation of intelligent medical implants capable of collecting and transmitting real-time physiological data. These advanced systems integrate miniature sensors, microelectronics, wireless communication modules, and biocompatible materials into orthopedic implants.

Unlike conventional implants, sensor-enabled orthopedic devices continuously monitor pressure, temperature, load distribution, strain, movement patterns, and biological indicators within the body. This real-time monitoring capability allows physicians to detect complications earlier, optimize rehabilitation programs, and improve implant longevity.

As healthcare systems worldwide shift toward preventive and personalized care models, smart orthopedic implants are becoming essential tools for improving surgical outcomes and reducing long-term treatment costs.

How Is Artificial Intelligence Reshaping the Implantable Sensor Orthopedic Market?

Artificial intelligence has emerged as one of the most influential technologies driving innovation across orthopedic care. AI-powered systems are helping healthcare providers convert vast amounts of sensor-generated data into clinically meaningful insights that support informed decision-making.

Advanced AI algorithms can predict implant complications before symptoms become apparent, enabling proactive interventions and reducing revision surgery rates. AI-assisted surgical planning has significantly improved implant sizing and placement accuracy, resulting in enhanced patient outcomes and reduced surgical risks.

Furthermore, AI-integrated orthopedic monitoring systems can continuously assess patient mobility, healing progression, and implant performance while generating personalized recovery recommendations. As healthcare providers increasingly embrace data-driven treatment models, AI-enabled implants are expected to become a cornerstone of future orthopedic care.

What Are the Major Growth Factors Fueling Market Expansion?

Rising Burden of Musculoskeletal Disorders

The increasing prevalence of osteoarthritis, osteoporosis, spinal disorders, and joint degeneration is creating sustained demand for advanced orthopedic implants capable of monitoring long-term patient health.

Growing Elderly Population

A rapidly aging global population is contributing to higher volumes of knee replacements, hip replacements, and spinal surgeries, directly supporting adoption of sensor-integrated implants.

Advances in Miniaturized Sensor Technologies

Breakthroughs in microelectromechanical systems (MEMS), nanoelectromechanical systems (NEMS), wireless communication, and battery-free sensors are improving implant performance while reducing device size.

Increasing Adoption of Remote Patient Monitoring

Healthcare providers are increasingly utilizing implantable sensors to support remote monitoring strategies, reducing hospital visits and improving long-term patient engagement.

Expansion of Robotic-Assisted Orthopedic Procedures

The integration of robotics and digital surgery platforms is creating new opportunities for sensor-enabled implants that provide real-time procedural feedback and post-operative monitoring.

Implantable Sensor Orthopedic Market Opportunities

The growing emphasis on personalized medicine is opening substantial opportunities for manufacturers developing next-generation implantable sensor technologies.

Smart implants can continuously collect patient-specific data, allowing physicians to customize rehabilitation programs, medication plans, and post-operative care pathways based on individual recovery patterns. This personalized approach improves therapeutic outcomes while reducing healthcare costs.

Moreover, integrating implantable sensors with smart drug delivery systems presents exciting possibilities for targeted therapies and precision medicine applications in orthopedic treatment.

Why Are MEMS and NEMS Technologies Becoming Critical to Future Growth?

Miniaturization remains one of the most important trends shaping the future of implantable orthopedic devices.

Advancements in MEMS and NEMS technologies are enabling the development of smaller, more efficient, and highly accurate sensors capable of functioning inside the human body for extended periods. These innovations are improving patient comfort while expanding clinical applications across joint replacement, spine surgery, trauma care, and rehabilitation monitoring.

As researchers continue to develop ultra-miniaturized sensing systems, manufacturers are expected to introduce increasingly sophisticated smart implants over the next decade.

Implantable Sensor Orthopedic Market Segmentation

Product Type Insights

The smart knee implants segment accounted for the largest market share of 45% in 2025. The segment’s dominance is attributed to the increasing number of knee replacement procedures and the rising prevalence of osteoarthritis. Embedded sensor technologies enable real-time monitoring of implant performance, improve post-operative recovery, reduce implant failures, and enhance patient outcomes. The growing adoption of robotic-assisted orthopedic surgeries further supports segment growth.

The smart hip implants segment captured 28% of the market share in 2025 and is projected to grow at a CAGR of 16.8% during the forecast period. Rising hip replacement surgeries, an aging population, and the ability of smart implants to improve rehabilitation and monitor implant longevity are driving market expansion.

The smart spinal implants segment held a 15% market share in 2025 and is expected to register the fastest CAGR of 18.9% through 2035. Increasing cases of spinal disorders, advancements in minimally invasive spine surgeries, and the growing demand for remote patient monitoring are fueling the segment’s rapid growth.

Product Type Revenue Outlook

| Product Type | 2025 Share | 2035 Share | CAGR |

| Smart Knee Implants | 45% | 47% | 18.1% |

| Smart Hip Implants | 28% | 27% | 16.8% |

| Smart Spinal Implants | 15% | 16% | 18.9% |

| Trauma & Extremity Implants | 8% | 7% | 15.4% |

| Others | 4% | 3% | 13.0% |

Sensor Type Insights

The pressure sensors segment led the market with a 34% share in 2025. Their widespread use in joint balancing, implant positioning, and real-time pressure monitoring during orthopedic procedures has strengthened market demand. These sensors also improve surgical precision while reducing infection risks.

The load and strain sensors segment accounted for 30% of the market in 2025 and is anticipated to grow at a CAGR of 18.5%. These sensors help measure implant stress, evaluate force transfer between implants and bones, and support personalized rehabilitation programs.

The multi-parameter sensors segment represented 8% of the market in 2025 and is projected to witness the fastest CAGR of 20.4% over the forecast period. Their ability to simultaneously monitor multiple physiological parameters, combined with AI-powered analytics, is driving their increasing adoption.

Technology Insights

Wireless sensor-enabled implants dominated the market with a 42% share in 2025. Their ability to transmit real-time patient data, improve treatment outcomes, and reduce hospital visits has accelerated adoption across orthopedic procedures.

Bluetooth-enabled implants held a 24% market share in 2025 and are expected to grow steadily at a CAGR of 14.8%. Smartphone connectivity, remote physician access, and increasing digital health adoption continue to support market growth.

AI-integrated monitoring implants accounted for 10% of the market in 2025 and are projected to expand at the fastest CAGR of 22.5%. Predictive analytics, personalized treatment planning, and early complication detection are major factors driving demand.

Application Insights

The joint replacement monitoring segment generated the highest market share of 38% in 2025. Rising arthroplasty procedures and the growing need to monitor implant performance, detect complications early, and reduce revision surgeries are supporting segment growth.

The post-operative recovery monitoring segment accounted for 23% of the market in 2025 and is expected to grow at a CAGR of 18.3%. Increasing adoption of remote patient monitoring, AI-enabled recovery tracking, and efforts to reduce hospital readmissions are contributing to market expansion.

The rehabilitation and mobility tracking segment held a 17% share in 2025 and is projected to grow at a CAGR of 19.4%. Rising demand for personalized rehabilitation, wearable sensor integration, and remote therapy monitoring continues to drive the segment.

Application Revenue Outlook

| Application | 2025 Share | 2035 Share | CAGR |

| Joint Replacement Monitoring | 38% | 39% | 17.9% |

| Post-operative Recovery Monitoring | 23% | 24% | 18.3% |

| Rehabilitation & Mobility Tracking | 17% | 18% | 19.4% |

| Infection Detection | 9% | 8% | 15.6% |

| Implant Performance Monitoring | 10% | 9% | 17.0% |

End User Insights

Hospitals dominated the implantable sensor orthopedic market with a 64% share in 2025. High volumes of orthopedic surgeries, advanced healthcare infrastructure, integrated patient monitoring systems, and favorable reimbursement policies have strengthened their market position.

Orthopedic specialty clinics captured 16% of the market in 2025 and are expected to grow at a CAGR of 18.4%, supported by increasing outpatient orthopedic procedures and digital patient management solutions.

Ambulatory surgical centers (ASCs) accounted for 11% of the market in 2025 and are projected to register the fastest CAGR of 20.1%. The growing preference for outpatient surgeries, lower treatment costs, and adoption of advanced surgical technologies are driving segment growth.

Implantable Sensor Orthopedic Market Regional Analysis

North America

North America dominated the implantable sensor orthopedic market with a 41% share in 2025. Early adoption of smart implants, advanced healthcare infrastructure, favorable reimbursement policies, and the presence of leading medical device manufacturers continue to drive regional growth.

U.S. Market

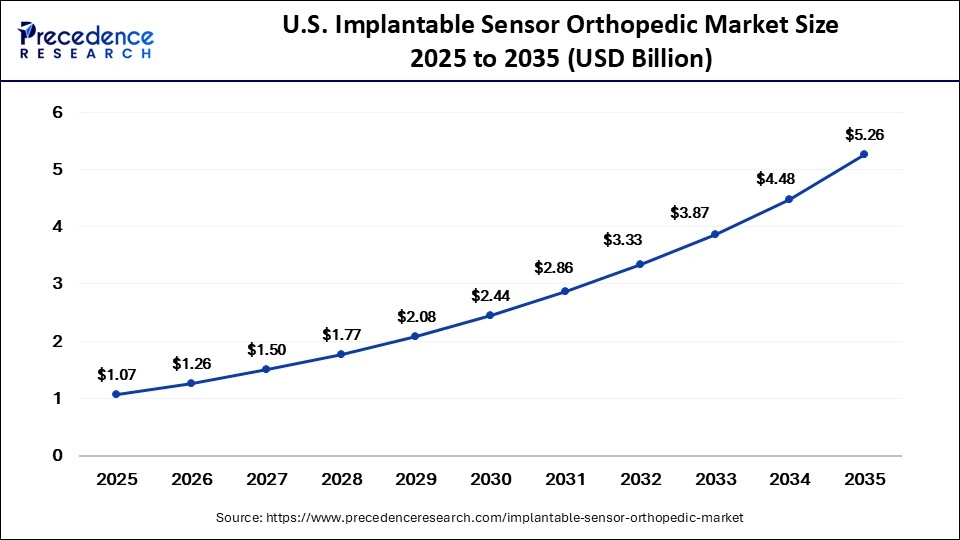

The U.S. remains the leading contributor to the regional market due to strong adoption of connected medical devices, increasing orthopedic procedures, and significant investments in biotechnology and medical device innovation.

The U.S. implantable orthopedic sensor market size reached USD 1.07 billion in 2025 and is expected to grow significantly to approximately USD 5.26 billion by 2035. The market is projected to expand at a CAGR of 15.93% between 2026 and 2035, driven by increasing adoption of smart orthopedic implants, advancements in sensor technologies, and growing demand for connected healthcare solutions.

Asia-Pacific

Asia-Pacific accounted for 22% of the market in 2025 and is expected to register the fastest CAGR of 21.2% through 2035. Rapid healthcare modernization, increasing musculoskeletal disorders, expanding orthopedic surgeries, and growing medical device manufacturing are accelerating regional growth.

China Market

China is emerging as a major growth market, supported by government healthcare initiatives, rising awareness of orthopedic health, and increasing demand for advanced implant technologies.

Europe

Europe held a 27% market share in 2025 and is projected to grow at a CAGR of 16.1%. An aging population, increasing joint replacement procedures, digital healthcare adoption, and government support for medical innovation are key growth drivers.

Germany Market

Germany is witnessing steady market expansion due to the growing use of minimally invasive orthopedic procedures, favorable regulatory support, and continuous advancements in orthopedic device technologies.

Middle East & Africa

The Middle East & Africa represented 5% of the market in 2025 and is expected to grow at a CAGR of 14.5%. Improving healthcare infrastructure, increasing orthopedic treatments, expanding medical tourism, and investments in specialty hospitals are supporting regional growth.

UAE Market

The UAE is experiencing strong growth due to technological advancements in implant sensor technologies, miniaturization of medical devices, and rising medical tourism.

Latin America

Latin America accounted for 6% of the global market in 2025 and is projected to grow at a CAGR of 14.8% during the forecast period. Expanding access to orthopedic care, rising sports injuries, and increasing adoption of advanced implants are contributing to market growth.

Brazil Market

Brazil remains one of the key regional markets, driven by increasing demand for advanced orthopedic surgeries, healthcare modernization, and the development of cost-effective implant technologies.

Implantable Sensor Orthopedic Market Key Players

Zimmer Biomet Holdings, Inc.

-

Persona IQ® (The Smart Knee): A commercially available, smart knee implant featuring a permanently embedded stem extension containing internal sensor hardware. It measures real-time post-operative patient kinematics, including range of motion, stride length, walking speed, and daily step count. Data is securely transmitted to a home base station and synchronized with the cloud-based mymobility® platform.

Stryker Corporation

-

Mako SmartRobotics™ & Structural Tech: Focuses on pre-operative 3D CT planning and intraoperative robotic guidance to optimize implant positioning and sizing. Digital tracking during the procedure relies on external optical arrays rather than permanently embedded diagnostic electronics inside the final prosthetic components.

Smith+Nephew plc

-

CORI† Surgical Robotic System & JOURNEY II: Employs the CORI robotic-assisted platform alongside the RI.KNEE ROBOTICS ecosystem. The system captures kinematic data during surgery using external optical tracker arrays and a digital tensioning mechanism to balance soft tissue, avoiding the use of active internal microelectronic sensors.

Johnson & Johnson MedTech (DePuy Synthes)

-

VELYS™ Digital Surgery Portfolio: Utilizes the VELYS Robotic-Assisted Solution and the VELYS Insights platform. Intraoperative planning and kinetic balancing are executed via dynamic, wireless external tracking arrays that interface with the surgical console. The final permanent orthopedic implants do not contain internal electronic sensors.

Medtronic plc

-

Mazor™ Robotics & UNiD™ Adaptive System (ASI): Digital technology footprint is centered on spinal surgery. The ecosystem utilizes the Mazor robotic guidance system and UNiD ASI software, which applies predictive artificial intelligence and adaptive spinal fixation hardware to optimize alignment, rather than utilizing telemetric electronic sensors.

Globus Medical, Inc.

-

ExcelsiusGPS® Platform: Focuses on musculoskeletal technology via the Excelsius ecosystem, providing computer-assisted navigation and rigid robotic guidance for spine and trauma procedures. Data tracking and surgical execution rely on external navigation arrays and specialized software workflows.

OrthoSensor, Inc.

-

VERASENSE™ Sensor-Embedded Tech: Specializes in disposable, wireless intraoperative sensor inserts. These microelectronic trial components are placed temporarily inside the joint space during a total knee replacement to provide real-time, quantitative data on joint load, alignment, and soft-tissue balance before final components are fixed.

Exactech, Inc.

-

Newton® Knee & Predict+®: Features the Newton Knee, an intraoperative, dynamic load-sensing platform that captures quantitative data on soft-tissue compliance throughout a full range of motion. This real-time surgical data feeds directly into Predict+, a machine-learning software application designed to predict personalized post-operative outcomes.

MicroPort Orthopedics Inc.

-

Evolution® Medial Pivot Knee System: Centers its orthopedic strategy around proprietary medial pivot implant geometries designed to replicate natural knee kinematics. Digital and precision planning are driven through advanced pre-operative mapping software and patient-specific instrumentation (PSI) rather than active electronics.

Conformis, Inc.

-

iFit® Image-to-Implant® Technology: Specializes in fully customized, patient-specific total knee and hip replacement systems. Utilizing patient CT scan data, proprietary 3D image-processing software designs bespoke femoral and tibial implants engineered to fit exact individual bone contours, utilizing personalized structural geometry instead of embedded electronic sensors.

NuVasive, Inc.

-

Pulse® Platform & MAGEC® System: Features the Pulse platform for integrated spine surgery workflows (neuromonitoring, global alignment, and navigation) alongside the MAGEC system. MAGEC consists of magnetically controlled, adjustable growing spinal rods that are mechanically lengthened non-invasively from outside the body via an external remote controller.

Orthofix Medical Inc.

-

PhysioStim™ & CervicalStim™ Platforms: Offers data-backed therapeutic systems focused on bone growth stimulation. These devices use targeted electromagnetic fields to promote bone healing post-surgery, featuring internal firmware that logs patient compliance and usage data for physician review.

Arthrex, Inc.

-

Synergy Sports Medicine Ecosystem: Focuses on connected surgical technology within sports medicine and arthroscopy. The sensor footprint is restricted to intraoperative device interfaces, including 4K visualization cameras, digital fluid management controllers, and automated surgical shaver systems.

Integra LifeSciences Holdings Corporation

-

Regenerative Orthopedics & Tissue Technologies: Focuses on advanced tissue technologies, dermal matrices, and specialized extremity reconstruction hardware (such as nerve conduits and tendon protection sleeves). The company does not develop active electronic or telemetric orthopedic hardware.

Smart Implant Solutions

-

Custom Prosthetic Interfaces: Specializes in the engineering and production of CAD/CAM customized prosthetic components, specialized interfaces, and structural attachment mechanisms within dental and specific orthopedic reconstructive fields. The portfolio is purely mechanical and structural, containing no active telemetric or diagnostic sensor hardware.

Recent Industry Developments Strengthening Market Momentum

Auxano Medical Expands Smart Implant Portfolio

- In June 2026, Auxano Medical launched a redesigned digital platform to provide broader access to its orthopedic implant technologies, including the ARKEO™ Wedge Fixation System and the INTREPED Intraosseous Fusion Device.

Ortho Development Commercializes Trivicta Hip Stem

- In May 2026, Ortho Development announced the nationwide commercial launch of its Trivicta Hip Stem, a cementless triple-taper femoral component designed for primary total hip arthroplasty procedures.

These developments reflect the growing industry focus on innovation, implant performance optimization, and enhanced patient outcomes.

Segments Covered in the Report

By Product Type

- Smart Knee Implants

- Smart Hip Implants

- Smart Spinal Implants

- Trauma & Extremity Implants

- Others

By Sensor Type

- Pressure Sensors

- Load & Strain Sensors

- Motion Sensors

- Temperature Sensors

- Multi-parameter Sensors

By Technology

- Wireless Sensor-enabled Implants

- Bluetooth-enabled Implants

- IoT-enabled Smart Implants

- AI-integrated Monitoring Implants

By Application

- Joint Replacement Monitoring

- Post-operative Recovery Monitoring

- Rehabilitation & Mobility Tracking

- Infection Detection

- Implant Performance Monitoring

- Others

By End User

- Hospitals

- Orthopedic Specialty Clinics

- Ambulatory Surgical Centers (ASCs)

- Research Institutes & Academic Centers

- Others

By Distribution Channel

- Direct Sales

- Medical Device Distributors

- Group Purchasing Organizations (GPOs)

- Tender Procurement

By Region

- North America

- Latin America

- Europe

- Asia-pacific

- Middle and East Africa

Read Also: U.S. Pharmaceutical Excipients Market Size to Reach USD 5.58 Billion by 2035

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/8499

You can place an order or ask any questions. Please feel free to contact us at sales@precedenceresearch.com |+1 804 441 9344

- Implantable Sensor Orthopedic Market Size to Reach USD 13.17 Billion by 2035 as AI-Powered Smart Implants Transform Orthopedic Care - June 19, 2026

- U.S. Pharmaceutical Excipients Market Size to Reach USD 5.58 Billion by 2035 Amid Rising Demand for Biologics and Advanced Drug Formulations - June 18, 2026

- Vietnam Kombucha Market Size to Surpass USD 113.18 Billion by 2035 Amid Rising Demand for Functional Beverages - June 17, 2026